GST launched: 1st July 2017 – India’s most significant indirect tax reform since Independence.

Key Objective: Unified system bringing multiple central & state taxes together → created a common national market.

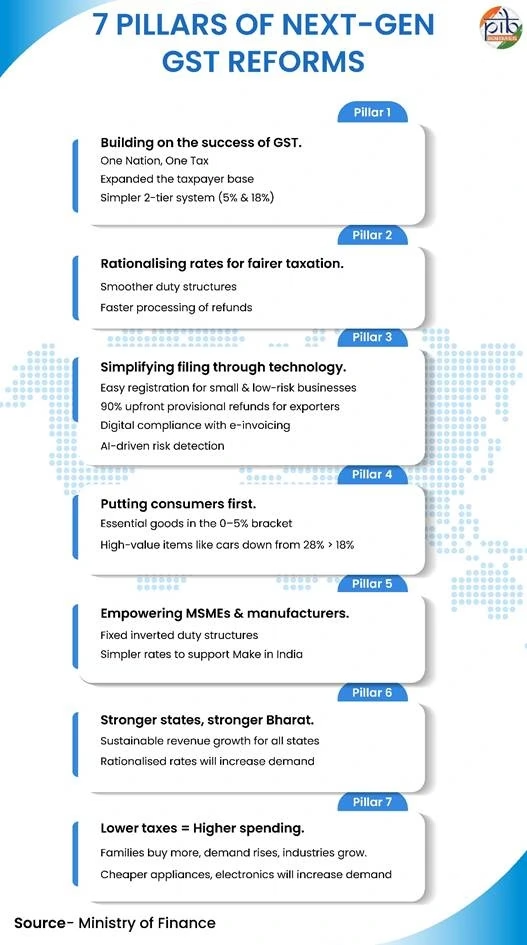

Benefits over 8 years:

- Cascading of taxes reduced.

- Simplified compliance.

- Improved transparency.

- Rate rationalisation & digitalisation.

- Became the backbone of India’s indirect tax framework.

56th GST Council Meeting (FM Nirmala Sitharaman): Approved Next-Generation GST reforms.

Food and Household Sector

- Reforms bring direct savings to households by reducing taxes on everyday essentials and packaged foods. GST rate cut on AC, Dishwashers and TVs (LCD, LED) is a dual win. It increases affordability for consumers while strengthening India’s electronics manufacturing ecosystem.

- Products like Ultra-High Temperature (UHT) milk, Pre-packaged and labelled chena or paneer, all the Indian Breads will see NIL rates

- Household goods like soaps, shampoos, toothbrushes, toothpaste, tableware, bicycles now at 5%.

- Food items such as packaged namkeens, Bhujia, Sauces, Pasta, Chocolates, Coffee, Preserved Meat etc. reduced from 12% OR 18% to 5%

- Consumer durables: TVs (LCD/LED) (> 32’), ACs, dishwashers: 28% → 18%.

Home Building & Materials

- The cut in GST on cement and construction materials will give a big boost to the housing sector. This will lower the cost of homes and infrastructure projects, making ownership of houses more affordable. The move is also expected to spur demand in real estate and create new jobs in construction.

- Cement: 28% → 18%.

- Marble/travertine blocks, Granite blocks, Sand-lime bricks: 12% → 5%

- Bamboo flooring / joinery, Packing cases & pallets (wood): 12% → 5%

Automobile Sector

- Clearer classification of vehicles and auto parts will cut down disputes, improve compliance, and support growth in India’s automotive manufacturing and exports.

- Small cars, two-wheelers ≤350cc: 28% → 18%.

- Buses, trucks, three-wheelers, all auto parts: 28% → 18%.

Agriculture sector

- Cheaper machinery and lower rates on bio-pesticides will help small farmers reduce costs and encourage sustainable farming practices. Correcting the inverted duty structure on Fertilizer inputs will boost domestic fertilizer production and reduce dependence on imports, strengthening self-reliance in agriculture.

- Tractors: 12% → 5%; tires and parts: 18% → 5%.

- Harvesters, threshers, sprinklers, drip irrigation, poultry & bee-keeping machines: 12% → 5%.

- Bio-pesticides and natural menthol: 12% → 5%.

Service sector

- Lower GST on hotel stays, gyms, salons, and yoga services will reduce costs for citizens, improve access to wellness, and give a fillip to the hospitality and service industries.

- Hotel stays up to ₹7,500/day from 12% to 5%.

- Gyms, salons, barbers, yoga GST cut from 18% to 5%.

Toys, Sports & Handicrafts

- Fixing duty structures for man-made fibres will improve the competitiveness of the textile industry, especially in exports. The inverted duty structure in the sector has been corrected with reduction of GST rate on manmade fibre from 18% to 5% and manmade yarn from 12% to 5%.

- Further, lower GST rates on handicrafts will support artisan livelihoods, preserve India’s cultural heritage, and promote rural economic growth.

- Handicraft idols & statues: 12% → 5%.

- Paintings, sculptures: 12% → 5%.

- Wooden/metal/textile dolls & toys: 12% → 5%.

Education Sector

- Education has become more affordable with exercise books, erasers, pencils, crayons and sharpeners moving to 0% GST. This directly supports families and students, ensuring lower costs of learning materials.

- Geometry boxes, school cartons, trays: 12% → 5%.

Medical Sector

- Reduced rates on medicines and medical devices will improve access to healthcare and support domestic manufacturing in the pharma and medical equipment sectors.

- 33 life-saving drugs, diagnostic kits: 12% → 0%.

- Other medicines including Ayurveda, Unani, Homoeopathy: 12% → 5%.

- Spectacles and corrective goggles: 28% → 5%.

- Medical oxygen, thermometers, surgical instruments: 12–18% → 5%.

- Medical, dental, and veterinary devices cut from 18% to 5%.

Health and life Insurance

- GST exemptions on life and health insurance premiums will expand financial protection and support the vision of Mission Insurance for All by 2047.

- GST exemption on premiums for individual life insurance, health insurance, floater plans, and senior citizen policies.

UPSC Spot-Check

Mains

The latest GST reforms mark a significant step towards simplification and fairness in India’s indirect tax regime. Discuss their potential impact on consumers, businesses, and government revenues.

(15 marks, 250 words)

Prelims

Consider the following statements:

Statement I: Under the latest GST reforms, luxury and sin goods such as pan masala, tobacco, aerated drinks, high-end cars, yachts, and private aircraft attract a 40% tax rate.

Statement II: Sin goods are taxed at higher rates because they are considered harmful to health or the environment, and higher taxation helps discourage consumption while generating revenue.

In the context of the above statements, which of the following is correct?

- Both Statement I and Statement II are correct and Statement II is the correct explanation of Statement I

- Both Statement I and Statement II are correct but Statement II is not the correct explanation of Statement I

- Statement I is correct but Statement II is incorrect

- Statement I is incorrect but Statement II is correct

At InclusiveIAS, our editorial team is led by experts who have successfully cleared multiple stages of the UPSC Civil Services Examination, including Mains and Interview. With deep insights into the demands of the exam, we focus on crafting content that is accurate, exam-relevant, and easy to grasp.

Whether it’s Polity, Current Affairs, GS papers, or Optional subjects, our notes are designed to:

Break down complex topics into simple, structured points

Align strictly with the UPSC syllabus and PYQ trends

Save your time by offering crisp yet comprehensive coverage

Help you score more with smart presentation, keywords, and examples

🟢 Every article, note, and test is not just written—but carefully edited to ensure it helps you study faster, revise better, and write answers like a topper.