Table of Contents

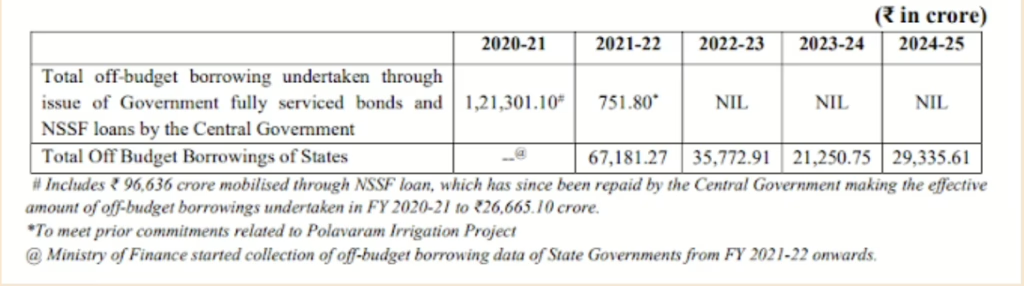

ToggleOff-budget borrowings refer to borrowings not directly made by the government (generally by public sector enterprises) but for which principal and interest are serviced from the government budget. It can be through various methods such as NSSF borrowings, domestic market borrowings, foreign market borrowings.

Facts

Central Government

State Government

The goal should be to move from opaque fiscal engineering to transparent and rules-based fiscal management. This aligns with global best practices (e.g., New Zealand’s Public Finance Act) and will strengthen India’s fiscal credibility, support higher sovereign ratings, and ensure sustainable development financing.

Sample UPSC Mains Question

Q. Off-budget borrowings, while helping governments meet fiscal and expenditure pressures, raise serious concerns regarding transparency and debt sustainability. Examine the rationale behind off-budget financing in India, its key methods, and the challenges it poses to fiscal governance. Suggest reforms to ensure greater accountability.

At InclusiveIAS, our editorial team is led by experts who have successfully cleared multiple stages of the UPSC Civil Services Examination, including Mains and Interview. With deep insights into the demands of the exam, we focus on crafting content that is accurate, exam-relevant, and easy to grasp.

Whether it’s Polity, Current Affairs, GS papers, or Optional subjects, our notes are designed to:

Break down complex topics into simple, structured points

Align strictly with the UPSC syllabus and PYQ trends

Save your time by offering crisp yet comprehensive coverage

Help you score more with smart presentation, keywords, and examples

🟢 Every article, note, and test is not just written—but carefully edited to ensure it helps you study faster, revise better, and write answers like a topper.